How to Write a Business Plan: Step-by-Step Guide + Examples

Noah Parsons

24 min. read

Updated May 7, 2024

Writing a business plan doesn’t have to be complicated.

In this step-by-step guide, you’ll learn how to write a business plan that’s detailed enough to impress bankers and potential investors, while giving you the tools to start, run, and grow a successful business.

- The basics of business planning

If you’re reading this guide, then you already know why you need a business plan .

You understand that planning helps you:

- Raise money

- Grow strategically

- Keep your business on the right track

As you start to write your plan, it’s useful to zoom out and remember what a business plan is .

At its core, a business plan is an overview of the products and services you sell, and the customers that you sell to. It explains your business strategy: how you’re going to build and grow your business, what your marketing strategy is, and who your competitors are.

Most business plans also include financial forecasts for the future. These set sales goals, budget for expenses, and predict profits and cash flow.

A good business plan is much more than just a document that you write once and forget about. It’s also a guide that helps you outline and achieve your goals.

After completing your plan, you can use it as a management tool to track your progress toward your goals. Updating and adjusting your forecasts and budgets as you go is one of the most important steps you can take to run a healthier, smarter business.

We’ll dive into how to use your plan later in this article.

There are many different types of plans , but we’ll go over the most common type here, which includes everything you need for an investor-ready plan. However, if you’re just starting out and are looking for something simpler—I recommend starting with a one-page business plan . It’s faster and easier to create.

It’s also the perfect place to start if you’re just figuring out your idea, or need a simple strategic plan to use inside your business.

Dig deeper : How to write a one-page business plan

Brought to you by

Create a professional business plan

Using ai and step-by-step instructions.

Secure funding

Validate ideas

Build a strategy

- What to include in your business plan

Executive summary

The executive summary is an overview of your business and your plans. It comes first in your plan and is ideally just one to two pages. Most people write it last because it’s a summary of the complete business plan.

Ideally, the executive summary can act as a stand-alone document that covers the highlights of your detailed plan.

In fact, it’s common for investors to ask only for the executive summary when evaluating your business. If they like what they see in the executive summary, they’ll often follow up with a request for a complete plan, a pitch presentation , or more in-depth financial forecasts .

Your executive summary should include:

- A summary of the problem you are solving

- A description of your product or service

- An overview of your target market

- A brief description of your team

- A summary of your financials

- Your funding requirements (if you are raising money)

Dig Deeper: How to write an effective executive summary

Products and services description

This is where you describe exactly what you’re selling, and how it solves a problem for your target market. The best way to organize this part of your plan is to start by describing the problem that exists for your customers. After that, you can describe how you plan to solve that problem with your product or service.

This is usually called a problem and solution statement .

To truly showcase the value of your products and services, you need to craft a compelling narrative around your offerings. How will your product or service transform your customers’ lives or jobs? A strong narrative will draw in your readers.

This is also the part of the business plan to discuss any competitive advantages you may have, like specific intellectual property or patents that protect your product. If you have any initial sales, contracts, or other evidence that your product or service is likely to sell, include that information as well. It will show that your idea has traction , which can help convince readers that your plan has a high chance of success.

Market analysis

Your target market is a description of the type of people that you plan to sell to. You might even have multiple target markets, depending on your business.

A market analysis is the part of your plan where you bring together all of the information you know about your target market. Basically, it’s a thorough description of who your customers are and why they need what you’re selling. You’ll also include information about the growth of your market and your industry .

Try to be as specific as possible when you describe your market.

Include information such as age, income level, and location—these are what’s called “demographics.” If you can, also describe your market’s interests and habits as they relate to your business—these are “psychographics.”

Related: Target market examples

Essentially, you want to include any knowledge you have about your customers that is relevant to how your product or service is right for them. With a solid target market, it will be easier to create a sales and marketing plan that will reach your customers. That’s because you know who they are, what they like to do, and the best ways to reach them.

Next, provide any additional information you have about your market.

What is the size of your market ? Is the market growing or shrinking? Ideally, you’ll want to demonstrate that your market is growing over time, and also explain how your business is positioned to take advantage of any expected changes in your industry.

Dig Deeper: Learn how to write a market analysis

Competitive analysis

Part of defining your business opportunity is determining what your competitive advantage is. To do this effectively, you need to know as much about your competitors as your target customers.

Every business has some form of competition. If you don’t think you have competitors, then explore what alternatives there are in the market for your product or service.

For example: In the early years of cars, their main competition was horses. For social media, the early competition was reading books, watching TV, and talking on the phone.

A good competitive analysis fully lays out the competitive landscape and then explains how your business is different. Maybe your products are better made, or cheaper, or your customer service is superior. Maybe your competitive advantage is your location – a wide variety of factors can ultimately give you an advantage.

Dig Deeper: How to write a competitive analysis for your business plan

Marketing and sales plan

The marketing and sales plan covers how you will position your product or service in the market, the marketing channels and messaging you will use, and your sales tactics.

The best place to start with a marketing plan is with a positioning statement .

This explains how your business fits into the overall market, and how you will explain the advantages of your product or service to customers. You’ll use the information from your competitive analysis to help you with your positioning.

For example: You might position your company as the premium, most expensive but the highest quality option in the market. Or your positioning might focus on being locally owned and that shoppers support the local economy by buying your products.

Once you understand your positioning, you’ll bring this together with the information about your target market to create your marketing strategy .

This is how you plan to communicate your message to potential customers. Depending on who your customers are and how they purchase products like yours, you might use many different strategies, from social media advertising to creating a podcast. Your marketing plan is all about how your customers discover who you are and why they should consider your products and services.

While your marketing plan is about reaching your customers—your sales plan will describe the actual sales process once a customer has decided that they’re interested in what you have to offer.

If your business requires salespeople and a long sales process, describe that in this section. If your customers can “self-serve” and just make purchases quickly on your website, describe that process.

A good sales plan picks up where your marketing plan leaves off. The marketing plan brings customers in the door and the sales plan is how you close the deal.

Together, these specific plans paint a picture of how you will connect with your target audience, and how you will turn them into paying customers.

Dig deeper: What to include in your sales and marketing plan

Business operations

The operations section describes the necessary requirements for your business to run smoothly. It’s where you talk about how your business works and what day-to-day operations look like.

Depending on how your business is structured, your operations plan may include elements of the business like:

- Supply chain management

- Manufacturing processes

- Equipment and technology

- Distribution

Some businesses distribute their products and reach their customers through large retailers like Amazon.com, Walmart, Target, and grocery store chains.

These businesses should review how this part of their business works. The plan should discuss the logistics and costs of getting products onto store shelves and any potential hurdles the business may have to overcome.

If your business is much simpler than this, that’s OK. This section of your business plan can be either extremely short or more detailed, depending on the type of business you are building.

For businesses selling services, such as physical therapy or online software, you can use this section to describe the technology you’ll leverage, what goes into your service, and who you will partner with to deliver your services.

Dig Deeper: Learn how to write the operations chapter of your plan

Key milestones and metrics

Although it’s not required to complete your business plan, mapping out key business milestones and the metrics can be incredibly useful for measuring your success.

Good milestones clearly lay out the parameters of the task and set expectations for their execution. You’ll want to include:

- A description of each task

- The proposed due date

- Who is responsible for each task

If you have a budget, you can include projected costs to hit each milestone. You don’t need extensive project planning in this section—just list key milestones you want to hit and when you plan to hit them. This is your overall business roadmap.

Possible milestones might be:

- Website launch date

- Store or office opening date

- First significant sales

- Break even date

- Business licenses and approvals

You should also discuss the key numbers you will track to determine your success. Some common metrics worth tracking include:

- Conversion rates

- Customer acquisition costs

- Profit per customer

- Repeat purchases

It’s perfectly fine to start with just a few metrics and grow the number you are tracking over time. You also may find that some metrics simply aren’t relevant to your business and can narrow down what you’re tracking.

Dig Deeper: How to use milestones in your business plan

Organization and management team

Investors don’t just look for great ideas—they want to find great teams. Use this chapter to describe your current team and who you need to hire . You should also provide a quick overview of your location and history if you’re already up and running.

Briefly highlight the relevant experiences of each key team member in the company. It’s important to make the case for why yours is the right team to turn an idea into a reality.

Do they have the right industry experience and background? Have members of the team had entrepreneurial successes before?

If you still need to hire key team members, that’s OK. Just note those gaps in this section.

Your company overview should also include a summary of your company’s current business structure . The most common business structures include:

- Sole proprietor

- Partnership

Be sure to provide an overview of how the business is owned as well. Does each business partner own an equal portion of the business? How is ownership divided?

Potential lenders and investors will want to know the structure of the business before they will consider a loan or investment.

Dig Deeper: How to write about your company structure and team

Financial plan

Last, but certainly not least, is your financial plan chapter.

Entrepreneurs often find this section the most daunting. But, business financials for most startups are less complicated than you think, and a business degree is certainly not required to build a solid financial forecast.

A typical financial forecast in a business plan includes the following:

- Sales forecast : An estimate of the sales expected over a given period. You’ll break down your forecast into the key revenue streams that you expect to have.

- Expense budget : Your planned spending such as personnel costs , marketing expenses, and taxes.

- Profit & Loss : Brings together your sales and expenses and helps you calculate planned profits.

- Cash Flow : Shows how cash moves into and out of your business. It can predict how much cash you’ll have on hand at any given point in the future.

- Balance Sheet : A list of the assets, liabilities, and equity in your company. In short, it provides an overview of the financial health of your business.

A strong business plan will include a description of assumptions about the future, and potential risks that could impact the financial plan. Including those will be especially important if you’re writing a business plan to pursue a loan or other investment.

Dig Deeper: How to create financial forecasts and budgets

This is the place for additional data, charts, or other information that supports your plan.

Including an appendix can significantly enhance the credibility of your plan by showing readers that you’ve thoroughly considered the details of your business idea, and are backing your ideas up with solid data.

Just remember that the information in the appendix is meant to be supplementary. Your business plan should stand on its own, even if the reader skips this section.

Dig Deeper : What to include in your business plan appendix

Optional: Business plan cover page

Adding a business plan cover page can make your plan, and by extension your business, seem more professional in the eyes of potential investors, lenders, and partners. It serves as the introduction to your document and provides necessary contact information for stakeholders to reference.

Your cover page should be simple and include:

- Company logo

- Business name

- Value proposition (optional)

- Business plan title

- Completion and/or update date

- Address and contact information

- Confidentiality statement

Just remember, the cover page is optional. If you decide to include it, keep it very simple and only spend a short amount of time putting it together.

Dig Deeper: How to create a business plan cover page

How to use AI to help write your business plan

Generative AI tools such as ChatGPT can speed up the business plan writing process and help you think through concepts like market segmentation and competition. These tools are especially useful for taking ideas that you provide and converting them into polished text for your business plan.

The best way to use AI for your business plan is to leverage it as a collaborator , not a replacement for human creative thinking and ingenuity.

AI can come up with lots of ideas and act as a brainstorming partner. It’s up to you to filter through those ideas and figure out which ones are realistic enough to resonate with your customers.

There are pros and cons of using AI to help with your business plan . So, spend some time understanding how it can be most helpful before just outsourcing the job to AI.

Learn more: 10 AI prompts you need to write a business plan

- Writing tips and strategies

To help streamline the business plan writing process, here are a few tips and key questions to answer to make sure you get the most out of your plan and avoid common mistakes .

Determine why you are writing a business plan

Knowing why you are writing a business plan will determine your approach to your planning project.

For example: If you are writing a business plan for yourself, or just to use inside your own business , you can probably skip the section about your team and organizational structure.

If you’re raising money, you’ll want to spend more time explaining why you’re looking to raise the funds and exactly how you will use them.

Regardless of how you intend to use your business plan , think about why you are writing and what you’re trying to get out of the process before you begin.

Keep things concise

Probably the most important tip is to keep your business plan short and simple. There are no prizes for long business plans . The longer your plan is, the less likely people are to read it.

So focus on trimming things down to the essentials your readers need to know. Skip the extended, wordy descriptions and instead focus on creating a plan that is easy to read —using bullets and short sentences whenever possible.

Have someone review your business plan

Writing a business plan in a vacuum is never a good idea. Sometimes it’s helpful to zoom out and check if your plan makes sense to someone else. You also want to make sure that it’s easy to read and understand.

Don’t wait until your plan is “done” to get a second look. Start sharing your plan early, and find out from readers what questions your plan leaves unanswered. This early review cycle will help you spot shortcomings in your plan and address them quickly, rather than finding out about them right before you present your plan to a lender or investor.

If you need a more detailed review, you may want to explore hiring a professional plan writer to thoroughly examine it.

Use a free business plan template and business plan examples to get started

Knowing what information to include in a business plan is sometimes not quite enough. If you’re struggling to get started or need additional guidance, it may be worth using a business plan template.

There are plenty of great options available (we’ve rounded up our 8 favorites to streamline your search).

But, if you’re looking for a free downloadable business plan template , you can get one right now; download the template used by more than 1 million businesses.

Or, if you just want to see what a completed business plan looks like, check out our library of over 550 free business plan examples .

We even have a growing list of industry business planning guides with tips for what to focus on depending on your business type.

Common pitfalls and how to avoid them

It’s easy to make mistakes when you’re writing your business plan. Some entrepreneurs get sucked into the writing and research process, and don’t focus enough on actually getting their business started.

Here are a few common mistakes and how to avoid them:

Not talking to your customers : This is one of the most common mistakes. It’s easy to assume that your product or service is something that people want. Before you invest too much in your business and too much in the planning process, make sure you talk to your prospective customers and have a good understanding of their needs.

- Overly optimistic sales and profit forecasts: By nature, entrepreneurs are optimistic about the future. But it’s good to temper that optimism a little when you’re planning, and make sure your forecasts are grounded in reality.

- Spending too much time planning: Yes, planning is crucial. But you also need to get out and talk to customers, build prototypes of your product and figure out if there’s a market for your idea. Make sure to balance planning with building.

- Not revising the plan: Planning is useful, but nothing ever goes exactly as planned. As you learn more about what’s working and what’s not—revise your plan, your budgets, and your revenue forecast. Doing so will provide a more realistic picture of where your business is going, and what your financial needs will be moving forward.

- Not using the plan to manage your business: A good business plan is a management tool. Don’t just write it and put it on the shelf to collect dust – use it to track your progress and help you reach your goals.

- Presenting your business plan

The planning process forces you to think through every aspect of your business and answer questions that you may not have thought of. That’s the real benefit of writing a business plan – the knowledge you gain about your business that you may not have been able to discover otherwise.

With all of this knowledge, you’re well prepared to convert your business plan into a pitch presentation to present your ideas.

A pitch presentation is a summary of your plan, just hitting the highlights and key points. It’s the best way to present your business plan to investors and team members.

Dig Deeper: Learn what key slides should be included in your pitch deck

Use your business plan to manage your business

One of the biggest benefits of planning is that it gives you a tool to manage your business better. With a revenue forecast, expense budget, and projected cash flow, you know your targets and where you are headed.

And yet, nothing ever goes exactly as planned – it’s the nature of business.

That’s where using your plan as a management tool comes in. The key to leveraging it for your business is to review it periodically and compare your forecasts and projections to your actual results.

Start by setting up a regular time to review the plan – a monthly review is a good starting point. During this review, answer questions like:

- Did you meet your sales goals?

- Is spending following your budget?

- Has anything gone differently than what you expected?

Now that you see whether you’re meeting your goals or are off track, you can make adjustments and set new targets.

Maybe you’re exceeding your sales goals and should set new, more aggressive goals. In that case, maybe you should also explore more spending or hiring more employees.

Or maybe expenses are rising faster than you projected. If that’s the case, you would need to look at where you can cut costs.

A plan, and a method for comparing your plan to your actual results , is the tool you need to steer your business toward success.

Learn More: How to run a regular plan review

Free business plan templates and examples

Kickstart your business plan writing with one of our free business plan templates or recommended tools.

Free business plan template

Download a free SBA-approved business plan template built for small businesses and startups.

Download Template

One-page plan template

Download a free one-page plan template to write a useful business plan in as little as 30-minutes.

Sample business plan library

Explore over 500 real-world business plan examples from a wide variety of industries.

View Sample Plans

How to write a business plan FAQ

What is a business plan?

A document that describes your business , the products and services you sell, and the customers that you sell to. It explains your business strategy, how you’re going to build and grow your business, what your marketing strategy is, and who your competitors are.

What are the benefits of a business plan?

A business plan helps you understand where you want to go with your business and what it will take to get there. It reduces your overall risk, helps you uncover your business’s potential, attracts investors, and identifies areas for growth.

Having a business plan ultimately makes you more confident as a business owner and more likely to succeed for a longer period of time.

What are the 7 steps of a business plan?

The seven steps to writing a business plan include:

- Write a brief executive summary

- Describe your products and services.

- Conduct market research and compile data into a cohesive market analysis.

- Describe your marketing and sales strategy.

- Outline your organizational structure and management team.

- Develop financial projections for sales, revenue, and cash flow.

- Add any additional documents to your appendix.

What are the 5 most common business plan mistakes?

There are plenty of mistakes that can be made when writing a business plan. However, these are the 5 most common that you should do your best to avoid:

- 1. Not taking the planning process seriously.

- Having unrealistic financial projections or incomplete financial information.

- Inconsistent information or simple mistakes.

- Failing to establish a sound business model.

- Not having a defined purpose for your business plan.

What questions should be answered in a business plan?

Writing a business plan is all about asking yourself questions about your business and being able to answer them through the planning process. You’ll likely be asking dozens and dozens of questions for each section of your plan.

However, these are the key questions you should ask and answer with your business plan:

- How will your business make money?

- Is there a need for your product or service?

- Who are your customers?

- How are you different from the competition?

- How will you reach your customers?

- How will you measure success?

How long should a business plan be?

The length of your business plan fully depends on what you intend to do with it. From the SBA and traditional lender point of view, a business plan needs to be whatever length necessary to fully explain your business. This means that you prove the viability of your business, show that you understand the market, and have a detailed strategy in place.

If you intend to use your business plan for internal management purposes, you don’t necessarily need a full 25-50 page business plan. Instead, you can start with a one-page plan to get all of the necessary information in place.

What are the different types of business plans?

While all business plans cover similar categories, the style and function fully depend on how you intend to use your plan. Here are a few common business plan types worth considering.

Traditional business plan: The tried-and-true traditional business plan is a formal document meant to be used when applying for funding or pitching to investors. This type of business plan follows the outline above and can be anywhere from 10-50 pages depending on the amount of detail included, the complexity of your business, and what you include in your appendix.

Business model canvas: The business model canvas is a one-page template designed to demystify the business planning process. It removes the need for a traditional, copy-heavy business plan, in favor of a single-page outline that can help you and outside parties better explore your business idea.

One-page business plan: This format is a simplified version of the traditional plan that focuses on the core aspects of your business. You’ll typically stick with bullet points and single sentences. It’s most useful for those exploring ideas, needing to validate their business model, or who need an internal plan to help them run and manage their business.

Lean Plan: The Lean Plan is less of a specific document type and more of a methodology. It takes the simplicity and styling of the one-page business plan and turns it into a process for you to continuously plan, test, review, refine, and take action based on performance. It’s faster, keeps your plan concise, and ensures that your plan is always up-to-date.

What’s the difference between a business plan and a strategic plan?

A business plan covers the “who” and “what” of your business. It explains what your business is doing right now and how it functions. The strategic plan explores long-term goals and explains “how” the business will get there. It encourages you to look more intently toward the future and how you will achieve your vision.

However, when approached correctly, your business plan can actually function as a strategic plan as well. If kept lean, you can define your business, outline strategic steps, and track ongoing operations all with a single plan.

See why 1.2 million entrepreneurs have written their business plans with LivePlan

Noah is the COO at Palo Alto Software, makers of the online business plan app LivePlan. He started his career at Yahoo! and then helped start the user review site Epinions.com. From there he started a software distribution business in the UK before coming to Palo Alto Software to run the marketing and product teams.

.png?format=auto "a full business plan should be written at the beginning of the entrepreneurial process")

Table of Contents

- Use AI to help write your plan

- Common planning mistakes

- Manage with your business plan

- Templates and examples

Related Articles

3 Min. Read

What to Include in Your Business Plan Appendix

1 Min. Read

How to Calculate Return on Investment (ROI)

5 Min. Read

How To Write a Business Plan for a Life Coaching Business + Free Example

7 Min. Read

How to Write a Bakery Business Plan + Sample

The Bplans Newsletter

The Bplans Weekly

Subscribe now for weekly advice and free downloadable resources to help start and grow your business.

We care about your privacy. See our privacy policy .

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

Want to create or adapt books like this? Learn more about how Pressbooks supports open publishing practices.

7 Entrepreneurial Process

Task Summary:

Lesson 3.1.1: The Entrepreneurial Process: Part 1

Lesson 3.1.2: The Entrepreneurial Process: Part 2

Lesson 3.1.3: Entrepreneurial Planning: Part 1

Lesson 3.1.4: Entrepreneurial Planning: Part 2

Lesson 3.1.5: Entrepreneurial Planning: Part 3

Activity 3.1.1: SDG Simulation

Unit 3 Assignment: Your Plan of Action

Learning Outcomes:

- Identify exciting entrepreneurial opportunities

- Evaluate exciting entrepreneurial opportunities

- Model the entrepreneurial process for the exciting entrepreneurial opportunities

- Create entrepreneurial planning documents

Successful entrepreneurship occurs when creative individuals bring together a new way of meeting needs and or wants. This is accomplished through a patterned process, one that mobilizes and directs resources to deliver a specific product or service to those in a way that is financially viable. While these could be 100% business ideas, they could also be concepts that are based in the spirit of altruism or non-profit. For innovative ideas that are strictly business concepts. sustainability can (and should) be embedded in the design of a product and operations by applying the criteria of reaching toward benign (or at least considerably safer) energy and material use, a reduced resource footprint, and elimination of inequitable social impacts due to the venture’s operations, including its supply-chain impacts.

Entrepreneurial innovation combined with sustainability principles can be broken down into the following four key elements, each of which requires analysis. Each one needs to be analyzed separately, and then the constellation of factors must fit together into a coherent whole. These four elements are as follows:

- Opportunity

- Entrepreneur/team

Successful ventures are characterized by coherence or “fit” across and throughout these steps. The interests and skills of the entrepreneur must fit with the product design and offering; the team’s qualifications should match the required knowledge needed to launch the venture. There needs to be a financially viable demand (enough people at a financially viable price) for the product or service, and of course, early adopters (those willing to purchase) have to be identified. Finally, sufficient resources, including financial resources (e.g., operating capital), office space, equipment, production facilities, components, materials, and expertise, must be identified and brought to bear. Each piece is discussed in more detail in the sections that follow.

Identify, Analyze, and Plan the Opportunity

As discussed in the last section, Opportunity Recognition is the active, cognitive process (or processes) through which individuals conclude that they have identified the potential to create something new that has the potential to generate economic value and that is not currently being exploited or developed and is viewed as desirable in the society in which it occurs (i.e. its development is consistent with existing legal and moral conditions). (Baron, 2004b, p. 52) Because opportunity recognition is a cognitive process, according to Baron (2004b), people can learn to be more effective at recognizing opportunities by changing the way they think about opportunities and how to recognize them.

The opportunity is a chance to satisfy the needs and desires of a certain group of people while generating returns that enable you to continue to operate and to build your organization over time. Many different conditions in society can create opportunities for new goods and services. As a prospective entrepreneur, the key questions are as follows:

- What is a need that is not being met?

- What are the conditions that have created an opportunity for my idea?

- Why do people want and need something new at this point in time?

- What are the factors that have opened up the opportunity?

- Will the opportunity be enduring, or is it a window that is open today but likely to close tomorrow?

- If you perceive an unmet need, can you deliver what the customer wants while generating durable margins and profits?

- How can I take on this venture while supporting the Sustainable Development Goals?

Opportunity conditions arise from a variety of sources. At a broad societal level, they are present as the result of forces such as shifting demographics, changes in knowledge and understanding due to scientific advances, a rebalancing or imbalance of political winds, or changing attitudes and norms that give rise to new needs. Certain demographic shifts and pollution challenges create SDG opportunities. When you combine enhanced public focus on health and wellness, advanced water treatment methods, clean combustion technologies, renewable “clean” energy sources, conversion of used packaging into new asset streams, benign chemical compounds for industrial processes, and local and sustainability has grown organic food, you begin to see the wide range of opportunities that exist due to macrotrends.

Identify, Analyze, and Plan the Market

What are you offering/doing/selling/contributing? New ventures offer solutions to people’s problems. This concept requires you to not only examine the item or service description but also further understand the group of people whose unmet needs you are meeting (often called market analysis). In any entrepreneurial innovation circumstance you must ask the following questions:

- What is the solution for which you want someone to pay?

- Is it a service or product, or some combination?

- To whom are you selling it? Is the buyer the actual user? Who makes the purchase decision?

- What is the customer’s problem and how does your service or product address it?

Understanding what you are selling is not as obvious as it might sound. When you sell an electric vehicle you are not just selling transportation. The buyer is buying a package of attributes that might include cutting-edge technology, lower operating costs, and perhaps the satisfaction of being part of a solution to health, environmental, and energy security problems.

Identify, Analyze, and Plan the Entrepreneur & Entrepreneurial Team

The opportunity and the entrepreneur must be intertwined in a way that optimizes the probability for success. People often become entrepreneurs when they see an opportunity. They are compelled to start something to find out whether they can convert that opportunity into an ongoing source of fulfillment and potential financial gain. That means that, ideally, the entrepreneur’s life experience, education, skills, work exposure, and network of contacts align well with the opportunity. We have covered this in previous sections, so if you need to refer back to consider the role of the entrepreneur’s skills, abilities, and cognition.

Entrepreneurs sometimes act alone, but this can only take us so far. A good entrepreneurial plan, an interesting product idea, and a promising opportunity are all positive, but in the end it is the ability of the entrepreneur to attract a team, get a product out, and provide it to customers is the thing that counts.

Typically there is an individual who initially drives the process through his or her ability to mobilize resources and sometimes through sheer force of will, hard work, and determination to succeed. In challenging times it is the entrepreneur’s vision and leadership abilities that can carry the day.

Ultimately, led by the entrepreneur, a team forms. As the organization grows, the team becomes the key factor. The entrepreneur’s skills, education, capabilities, and weaknesses must be augmented and complemented by the competencies of the team members they bring to the project. The following are important questions to ask:

- Does the team as a unit have the background, skills, and understanding of the opportunity to overcome obstacles?

- Can the team act as a collaborative unit with strong decision-making ability under fluid conditions?

- Can the team deal with conflict and disagreement as a normal and healthy aspect of working through complex decisions under ambiguity?

If an organization has been established and the team has not yet been formed, these questions will be useful to help you understand what configuration of people might compose an effective team to carry the business through its early evolutionary stages.

Identify, Analyze, and Plan the Resources

Successful entrepreneurial processes require entrepreneurs and teams to mobilize a wide array of resources quickly and efficiently. All innovative and entrepreneurial ventures combine specific resources such as capital, talent and know-how (e.g., accountants, lawyers), equipment, and production facilities. Breaking down an opportunity’s required resources into components can clarify what is needed and when it is needed. Although resource needs change during the early growth stages of an opportunity, at each stage the entrepreneur should be clear about the priority resources that enable or inhibit moving to the next stage of growth. What kinds of resources are needed? The following list provides guidance:

- Capital. What financial resources, in what form (e.g., equity, debt, family loans, angel capital, venture capital), are needed at the first stage? This requires an understanding of cash flow needs, break-even time frames, and other details. Even non-profits need to make money to stay afloat. Back-of-the-envelope estimates must be converted to pro forma income statements to understand financial needs.

- Know-how. Record keeping and accounting and legal process and advice are essential resources that must be considered at the start of every venture. Access to experts is important, especially in the early stages of making an opportunity happen. New opportunities require legal incorporation, financial record keeping, and rudimentary systems and resources to provide for these expenses need to be considered.

- Facilities, equipment, and transport. Does the venture need office space, production facilities, special equipment, or transportation? At the early stage of analysis, ownership of these resources does not need to be determined. The resource requirement, however, must be identified.

The Overall Process

The process of entrepreneurship melds these pieces together in processes that unfold over weeks and months, and eventually years if the business is successful. Breaking down the process into categories and components helps you understand the pieces and how they fit together. What we find in retrospect with successful launches is a cohesive fit among the parts. The entrepreneur’s skills and education match what the start-up needs. The opportunity can be optimally explored with the team and resources that are identified and mobilized. The resources must be brought to bear to launch the opportunity with an entry strategy that delivers the value-driven concept in a way that solves customers’ problems.

With all of these things in mind, documenting answers to the questions above, and the analysis undertaken to answer them is contained in an entrepreneurial plan. This is a document that you would use to plan out the details for the elements outlined above. Making sure you identify, analyze, and plan these elements is a great starting point, and to make sure this is all done really well, have a look at the principles below.

Entrepreneurial Plan Communication Principles

As Hindle and Mainprize (2006) note, business plan writers must strive to communicate their expectations about the nature of an uncertain future. However, the liabilities of newness make communicating the expected future of new opportunities difficult (more so than for existing organizations). They outline five communications principles:

- Translation of your vision of the venture and how it will perform into a format compatible with the expectations of the readers

- you have identified and understood the key success factors and risks

- the projected market is large and you expect good market penetration

- you have a strategy for commercialization, profitability, and market domination

- you can establish and protect a proprietary and competitive position

- Anchoring key events in the plan with specific financial and quantitative values

- your major plan objectives are in the form of financial targets

- you have addressed the dual need for planning and flexibility

- you understand the hazards of neglecting linkages between certain events

- you understand the importance of quantitative values (rather than just chronological dates)

- Nothing lasts forever—things can change to impact the opportunity: tastes, preferences, technological innovation, competitive landscape

- the new combination upon which venture is built

- the magnitude of the opportunity or market size

- market growth trends

- venture’s value from the market (% of market share proposed or market share value in dollars)

- Four key aspects describing context within which new opportunity is intended to function (internal and external environment)

- how the context will help or hinder the proposal

- how the context may change and affect the organization and the range of flexibility or response that is built into the venture

- what management can or will do in the event the context turns unfavorable

- what management can do to affect the context in a positive way

- A brief and clear statement of how an idea actually becomes a business that creates value

- Who pays, how much, and how often?

- The activities the company must perform to produce its product, deliver it to its customers, and earn revenue

- And be able to defend assertions that the venture is attractive and sustainable and has a competitive edge

Entrepreneurial Plan Credibility Principles

Entrepreneurial plan writers must strive to project credibility (Hindle & Mainprize, 2006), so there must be a match between what the entrepreneurship team (resource seekers) needs and what the resource providers expect based on their criteria. A take it or leave it approach (i.e. financial forecasts set in concrete) by the entrepreneurship team has a high likelihood of failure in terms of securing resources. Hindle and Mainprize (2006) outline five principles to help entrepreneurs project credibility:

- Without the right team, nothing else matters.

- What do they know?

- Who do they know?

- How well are they known?

- sub-strategies

- ad-hoc programs

- specific tactical action plans

- Claiming an insuperable lead or a proprietary market position is naïve.

- Anticipate several moves in advance

- View the future as a movie vs. snapshot

- Key assumptions related to market size, penetration rates, and timing issues of market context outlined in the entrepreneurial plan should link directly to the financial statements.

- Income and cash flow statements must be preceded by operational statements setting forth the primary planning assumptions about market sizes, sales, productivity, and basis for the revenue estimate.

- If the main purpose is to enact a harvest, then the entrepreneurial plan must create a value-adding deal structure to attract investors.

- Common things: viability, profit potential, downside risk, likely life-cycle time, potential areas for dispute or improvement

General Entrepreneurial Plan Guidelines

Many entrepreneurs must have a plan to achieve their goals. The following are some basic guidelines for entrepreneurial plan development.

- A standard format helps the reader understand that the entrepreneur has thought everything through and that the returns justify the risk.

- Binding the document ensures that readers can easily go through it without it falling apart.

- everything is completely integrated: the written part must say exactly the same thing as the financial part

- all financial statements are completely linked and valid (make sure all balance sheets validly balance)

- the document is well-formatted (layout makes the document easy to read and comprehend—including all diagrams, charts, statements, and other additions)

- everything is correct (there are NO spelling, grammar, sentence structure, referencing, or calculation errors)

- It is usually unnecessary—and even damaging—to state the same thing more than once. To avoid unnecessarily duplicating information, you should combine sections and reduce or eliminate duplication as much as possible.

- all the necessary information is included to enable readers to understand everything in your document

- For example, if your plan says something like “there is a shortage of 100,000 units with competitors currently producing 25,000. We can help fill this huge gap in demand with our capacity to produce 5,000 units,” a reader is left completely confused. Does this mean there is a total shortage of 100,000 units, but competitors are filling this gap by producing 25,000 per year (in which case there will only be a shortage for four years)? Or, is there an annual shortage of 100,000 units with only 25,000 being produced each year, in which case the total shortage is very high and is growing each year? You must always provide the complete perspective by indicating the appropriate time frame, currency, size, or another measurement.

- if you use a percentage figure, you indicate to what it refers, otherwise, the figure is completely useless to a reader.

- This can be solved by indicating up-front in the document the currency in which all values will be quoted. Another option is to indicate each time which currency is being used, and sometimes you might want to indicate the value in more than one currency. Of course, you will need to assess the exchange rate risk to which you will be exposed and describe this in your document.

- If a statement is included that presents something as a fact when this fact is not generally known, always indicate the source. Unsupported statements damage credibility

- Be specific. An entrepreneurial plan is simply not of value if it uses vague references to high demand, carefully set prices, and another weak phrasing. It must show hard numbers (properly referenced, of course), actual prices, and real data acquired through proper research. This is the only way to ensure your plan is considered credible.

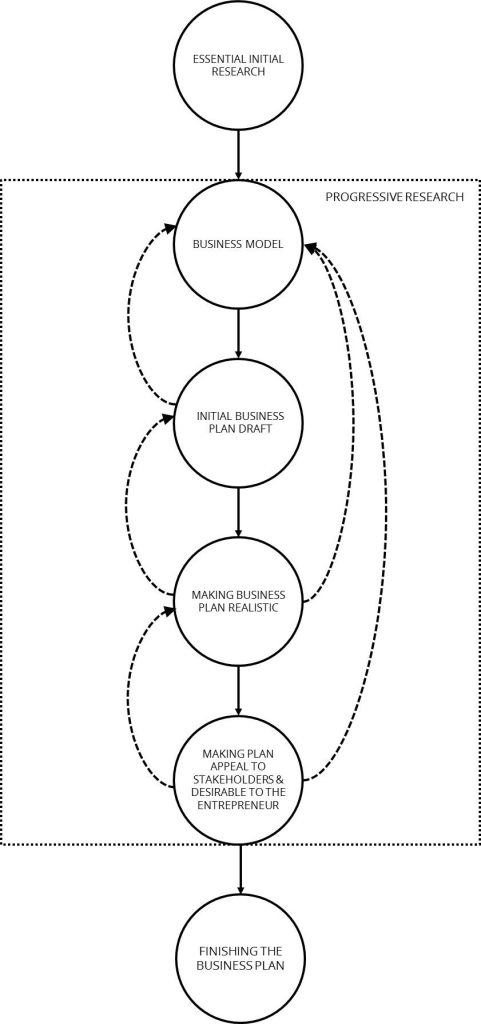

The purpose of this assignment is to connect all of the dots that you have been learning about and engaging with over the past unit when it comes to the entrepreneurial planning process. Watch this video on developing a process map . You are going to develop your own process map outlining the steps you need to take to develop a robust and well-thought-out entrepreneurial plan. Have a look at the Unit 4 Assignment: Entrepreneurial Plan for more information on what you’re going to be building.

The submission should be methodical and outline the process you will go through (i.e. what steps you will complete), and the information sources you will need to fill in the gaps and fill out your plan. Your submission should include a process map diagram, and be about 250 words, which is one page double spaced, or it could be done as an infographic, or a two-three minute presentation. If you are doing this as part of a formal course and have a different approach that you would like to take for developing this assignment, please check with your instructor.

Text Attributions

The content related to how it all starts and the process steps was taken from “ Sustainability, Innovation, and Entrepreneurship” by LibreTexts (2020) CC BY-NC-SA

The content related to the opportunity identification cognition and the entrepreneurial plan was taken from “ Entrepreneurship and Innovation Toolkit, 3rd Edition ” by L. Swanson (2017) CC BY-SA

Baron, R. A. (2004b). Opportunity recognition: Insights from a cognitive perspective. In J. E. Butler (Ed.), Opportunity identification and entrepreneurial behavior (pp. 47-73). Greenwich, Conn.: Information Age Pub

Hindle, K., & Mainprize, B. (2006). A systematic approach to writing and rating entrepreneurial business plans. The Journal of Private Equity, 9 (3), 7-23.

Introduction to Entrepreneurship Copyright © 2021 by Katherine Carpenter is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License , except where otherwise noted.

Share This Book

A business journal from the Wharton School of the University of Pennsylvania

Knowledge at Wharton Podcast

How entrepreneurs can create effective business plans, march 2, 2010 • 16 min listen.

When an entrepreneur has identified a potential business opportunity, the next step is developing a business plan for the new venture. What exactly should the new plan contain? How can the entrepreneur ensure it has the substance to find interest among would-be investors? In this installment of a series of podcasts for the Wharton-CERT Business Plan Competition, Wharton management professor Ian MacMillan explains that business plans must contain several crucial elements: They must articulate a market need; identify products or services to fill that need; assess the resources required to produce those products or services; address the risks involved in the venture; and estimate the potential revenues and profits.

An edited transcript of the interview appears below:

Knowledge at Wharton: Professor MacMillan, thank you for speaking with us about the necessity of entrepreneurs writing business plans. To start with a basic question, what exactly is a business plan?

Ian MacMillan: A business plan to me is a 25-page, maximum 30-page, document, which is a description, analysis and evaluation of a venture that you want to get funded by somebody. It provides critical information to the reader — usually an investor — about you, the entrepreneur, about the market that you are going to enter, about the product that you want to enter with, your strategy for entry, what the prospects are financially, and what the risks are to anybody who invests in the project.

Knowledge at Wharton: Could you explain some of these elements in a little more detail and describe how entrepreneurs can develop an effective business plan?

MacMillan: Let me start by saying that you probably want to avoid developing a detailed business plan unless you have done some initial work. Basically what happens is that by doing a little bit of work, you earn the right to do more work. The first thing I would do before you start a business plan is think about a concept statement. A concept statement is about three to five pages that you put together and share with potential customers or investors just to see if they think it’s worth the energy and effort of doing more detailed work.

The concept statement has a few pieces to it. You are going to have a description of the market need that has to be fulfilled; a description of the products or services that you think are going to fulfill that need; a description of the key resources that you think are going to be needed to provide that product or service; a specification of what resources are currently available; an articulation of what you think the risks are; and then a sort of rough and ready estimate of what you think the profits and profitability will be.

The idea is to put together this concept document and begin to share it around with people who are going to have to support your venture if you take it forward. This allows you to rethink as a result of feedback that you get. You might get word back from the various stakeholders — like potential customers or distributors — that this really wasn’t such a good idea after all. That saves you the energy and effort of putting together a big business plan.

Knowledge at Wharton: Assuming the concept statement works out and you want to move towards the business plan, what else would you need? And where can you find the information? Some information can be hard to locate, especially about your competitors.

MacMillan: It’s really important to go out and speak to your potential customers. You need to find the people who you think will buy your product and talk to them about what dissatisfies them with their current offerings. You should get a sense from them about who is providing the alternative at the moment. Remember, the world has gone for maybe 100,000 years without your idea — and people are getting by; they’re not dying. Something out there is servicing their need. So what is the closest competitive alternative to what you want to offer?

That is what you need to find out — and that involves talking and listening. And for all the enthusiasm you have for your venture or your idea, you really need to listen to people who are eventually going to write a check for it.

Before you go on to write a business plan, you have to do some more work. If the concept statement looks good, then the next step is to do a 15- to 20-page feasibility analysis. This means we are now going to take this idea to the next level. We’ve learned from potential customers and distributors. We’ve learned who the major competitors are. We’ve shaped the idea more clearly, and now we’re digging deeper.

The next challenge you face is to say, well, if you start this business, what evidence do you have that the market actually wants it? Who do you think would write a check for your product? You need to articulate what makes your product or your service feasible. What has to be done in order to make this thing real? You need a description of how you intend to enter the market, a description of who the major competitors are, a preliminary plan — a very rough plan — which specifies what you think your revenues and profits are going to be, and an estimate of what you think the required investment will be. And only then, once you have articulated that, and once again shared it with your stakeholder community, will you perhaps be able to go and write a business plan.

Knowledge at Wharton: Once you have done your feasibility analysis and assuming you get the go ahead from your stakeholders, what is the next step?

MacMillan: The idea of the business plan is to convince the stakeholders. First, what we need to do in a business plan is show that we understand the needs — the unmet needs — of potential customers. Second, we need to understand the strengths and weaknesses of the current most competitive offering out there. Third, we need to understand the skills and capabilities that you and your team have as entrepreneurs. Next we need to understand what the investors need to get out of their investment, because they have to put their money in and they need to have some kind of sense of what they are going to get in terms of returns. In addition, the investment needs to be competitive with alternative investments that the investors might make.

The most important idea in the business plan is to articulate and satisfy the different perspectives of various stakeholders. This process sets in motion some basic requirements in the business plan — to tee up right from the start — evidence that the customer will accept it. Probably a third of the ventures out there that fail are because some person came up with the right product that they thought the world would love and then found out that the customers couldn’t care less. What you want to try to do in a business plan is convince the reader that there are customers out there who will in fact buy the product — not because it’s a great product, but because they want it and they are willing to pay for it.

Moreover, you need to convince the reader that you have some kind of proprietary position that you can defend. You also need to convince your readers that you have an experienced and motivated management team and that you have the experience and the management capabilities to pull it off. You need to convince potential investors that they are going to get a better return than they could get elsewhere, so you need to estimate the net present value of this venture. You need to show that the risk they are taking will be accompanied by appropriate returns for that risk. If we look at the contents of a typical business plan, you need to be able to articulate all these issues in some 25 to 30 pages. People get tired if they have to read too much.

Now let’s look at the various components of the business plan document:

First, you need an executive summary that grabs the attention of the potential investor. This should be done in no more than two pages. The executive summary is meant to convince the potential investor to read further and say, “Wow! This is why I should read more about this business plan.”

Next, you need a market analysis. What is the market? How fast is it growing? How big is it? Who are the major players? In addition, you need a strategy section. It should address questions such as, “How are you going to get into this market? And how are you going to win in that marketplace against current competition?”

After that, you need a marketing plan. How are we going to segment the market? Which parts of the market are we going to attack? How are we going to get the attention of that market and attract it to our product or service?

You also need an operations plan that answers the question, “How are we going to make it happen?” And you need an organization plan, which shows who the people are who will take part in the venture.

You need to list the key events that will take place as the plan unfolds. What are the major things that are going to happen? If your plan happens to be about a physical product, are you going to have a prototype or a model? If it happens to be a software product, are you going to have a piece of software developed — a prototypical piece of software? What are the key milestones by which investors can judge what progress you are making in the investment? Remember that you will not get all your money up front. You will get your funds allocated contingent on your ability to achieve key milestones. So you may as well indicate what those milestones are.

You should also include a hard-nosed assessment of the key risks. For example, what are the market risks? What are the product risks? What are the financial risks? What are the competitive risks? To the extent that you are upfront and honest about it, you will convince your potential investors that you have done your homework. You need to also be able to indicate how you will mitigate these risks — because if you can’t mitigate them, investors are not going to put money into your venture.

After that, what you get down to is a financial plan where you basically do a five-year forecast of what you think the finances are going to be — maybe with quarterly data or projections for the first two years and annual for the next three years.

You need a pro forma profit and loss statement. You need a pro forma balance sheet if you have assets in the balance sheet. You need to have a pro forma cash flow. Your cash flow is important, because it is the cash flow that kills. You may have great profits on your books but you may run out of money — so you need a pro forma cash flow statement. And you need a financing plan that explains, as the project unfolds, what tranches of financing you will need and how will you go about raising that money.

Finally you need a financial evaluation that tells investors, if you make this investment, what is its value going to be to you as an investor. That is basically the structure of the plan.

Knowledge at Wharton: Let’s say you have written a business plan and presented it to your investors. How closely do you have to be tied to the plan? Does it mean that once you are executing against the plan, you should reject new opportunities you find because they are not part of your plan? Or should you build in some flexibility that allows you to explore emerging opportunities?

MacMillan: Is this an opportunity for me to speak about discovery-driven planning?

Knowledge at Wharton: Of course.

MacMillan: Okay. The thing about most entrepreneurial ventures is that your outcome is uncertain — because what you are doing is very new. It is very, very hard to predict what the actual outcome is going to be. One of the most fundamental flaws is that in the face of unfolding uncertainty, you single-mindedly and bloody-mindedly pursue the original objective.

The reality is that the true opportunity will emerge over time. What venture capitalists do is they will put a small amount of money into the project, allow the entrepreneur to enter that market space and then — contingent on performance and contingent on what apparent traction you can get in that market space — completely re-plan to find out what the true opportunity really is. It is insanity to insist that people actually meet their plan as it was originally written.

This doesn’t mean you compromise your objectives. The idea is that I want to keep on trying to meet my objectives, but how I meet them must change as the plan unfolds. That’s basically what led to all the work that Wharton has done in the last few years on discovery driven planning. It’s a way of thinking about planning that says, “I’m going to make small investments. If I’m wrong early, I can fail fast, fail cheap and move on. But as I find out what the true opportunity is, I can aggressively invest in what this opportunity is.”

Knowledge at Wharton: Could you give an example of a company that has used this discovery-driven planning process to take its business to the next level?

MacMillan: One company that has done the most in this area is Air Products. What they have been able to do is use discovery-driven planning to unfold completely different businesses from the ones that they were in. Air Products makes things like carbon dioxide and oxygen and nitrogen. It is a very old-line company. Using discovery-driven planning, they have been able to move aggressively into, for instance, the service sector. Once they recognized that they were able to deliver reliably and predictably in the face of uncertain demand, they developed a set of skills that allowed them to enter the service business where the return on investment and return on assets are far higher than putting a huge plant in place.

Knowledge at Wharton: Professor MacMillan, thanks so much.

More From Knowledge at Wharton

How Financial Frictions Hinder Innovation

How Early Adopters of Gen AI Are Gaining Efficiencies

How Is AI Affecting Innovation Management?

Looking for more insights.

Sign up to stay informed about our latest article releases.

Business Plan Development

Masterplans experts will help you create business plans for investor funding, bank/SBA lending and strategic direction

Investor Materials

A professionally designed pitch deck, lean plan, and cash burn overview will assist you in securing Pre-Seed and Seed Round funding

Immigration Business Plans

A USCIS-compliant business plan serves as the foundation for your E-2, L-1A, EB-5 or E-2 visa application

Customized consulting tailored to your startup's unique challenges and goals

Our team-based approach supports your project with personal communication and technical expertise.

Pricing that is competitive and scalable for early-stage business services regardless of industry or stage.

Client testimonials from just a few of the 18,000+ entrepreneurs we've worked with over the last 20 years

Free tools, research, and templates to help with business plans & pitch decks

Writing a Solid Business Plan: Fundamentals and Principles

I’ve worked as a business plan writer since 2006, and it’s been a remarkably fun and fulfilling career for me. I get to see entrepreneurs of all sorts, from all over the world, live out their dreams.

When I’m out and about meeting people in the real world, I don’t dread the question, “What do you do for a living,” like some people do, because I love talking about what I do for a living.

But what I am quite used to is the blank stare that I tend to get, and the follow-up question, “What does that mean?” Other people nod their heads knowingly, especially if they have some experience with business or finance, but once they ask subsequent questions I realize they’re thinking of something completely different. So, I thought it might be helpful to talk about the top questions the Masterplans team gets about business plan writing and what happens when you hire a business plan writer.

What even is a business plan?

The most basic possible question, and what people really mean when they ask me what my job title really means. I love to answer this question, except when I’m trying to explain it to relatives in Greece, or my Spanish-speaking friends! My second- and third-language skills are not strong enough to begin to explain what a business plan is. But, when I try to explain it to them, I break it down into the simplest terms, so maybe that’s the best place to start here. I do this with a series of questions and statements that go like this:

- Have you ever thought about starting your own business? (Inevitably, the answer is yes)

- Well, when you want to start your own business, you will probably need to apply for a loan, or ask an investor for funding. (People nod at this one… I’ve still got their comprehension).

- When you do that, you need to present a document that tells all about the business you’re starting. I write that document.

And bingo, we have a basic level of understanding of what I do. But of course, it’s so much more complicated than that . A traditional business plan is made up of a complete outline of topics and sub-topics that any entrepreneur needs to be able to answer. It’s not always about funding either, even though that’s how I present it to friends. The truth is that every entrepreneur needs a business plan, even if they’re bootstrapping the project out of their own pocket.

In actuality, a business plan is a comprehensive document that explains the details about your business, sets goals and objectives, and guides you going forward. That said, if you are pursuing funding like most entrepreneurs, your document needs to cover a range of required topics.

Let’s take a look at the SBA requirements for the sections that need to be in a business plan:

- Executive Summary

- Company Description

- Market Analysis

- Organization and Management

- Service or Product line

- Marketing and Sales

- Funding request

- Financial projections

- Appendix (optional)

However, this is an overly broad listing, which doesn’t include many of the sub-sections that are involved. For example, at Masterplans, our Market Analysis covers a variety of sub-sections like Market Segmentation, Market Need, Industry Analysis, Competitive Comparison, and Competitive Edge.

Part of being a good business plan writer means understanding what goes within each section and keeping the content organized into the appropriate area. Some customers have a hard time keeping straight the difference between the "Competitive Comparison" and the "Competitive Edge" sections, but they are quite distinct. Or, it can be tempting to talk about who your customers are in the "Market Analysis" instead of the "Market Segmentation." I’ve even had people mix up marketing tactics with products or services. It takes an experienced hand to keep the content organized.

What is the purpose of a business plan?

A business plan’s highest purpose is to guide entrepreneurs in operating their business on the day-to-day level. It is a foundational document that I think of as the constitution of your business. It tells you everything you need to know about your idea, your goals, your strategy, and the financial picture of a business.

Here at Masterplans, we strongly believe that entrepreneurs need to understand that a business plan is not a one-time use product, like applying for a business loan. Instead, we want our clients to use their business plan all the time, for years into the future, as long as the business exists. It should guide board meetings and management decisions. Your employees should read it so that they understand what your mission is, what steps you need to take to achieve success, and what their role is within your company.

But we admit that there are those one-time, single-serving uses for a business plan that will likely come up for you. You need it to apply for a bank loan. You need it to ask for investment. You need it when applying for a lease on a location. You often need it when applying for certain permits, especially those dealing with compliance issues. And for those of you who are foreign investors seeking a visa , you need it to include in your application packet to USCIS.

Thus, a comprehensive business plan needs to be able to not just guide you in your daily decision-making, but it also needs to answer all the questions that an outside party might ask you when deciding whether to fund your idea or let you lease their space.

Who should write a business plan?

Why, the entrepreneurial team should take the helm in writing a business plan, of course. Did you expect a different answer from a professional business plan writer? At Masterplans, we don’t shy away from delivering honest truth to our clients, because we thrive when they thrive.

The truth is that an entrepreneur who isn’t intimately involved in the writing of their business plan from the start will never fully understand it, and that can hamper them on their path to achieving their goals. It’s imperative that an entrepreneur have a deep understanding of their business plan, or else they won’t be able to follow it!

But, writing a business plan is an intense endeavor that requires a better-than-average command of English writing and style, as well as business theory and financial modeling. Very few people represent the total package, which is why at Masterplans, we work in teams of specialists who together have those skills.

I can write a beautiful market analysis summary, analyze your competitive landscape in-depth, and wrap it all up with an attention-grabbing executive summary, but don’t ask me to explain a complex financial concept like Internal Rate of Return. (I’m being modest; I can tell you all about it, but I’ll leave that to our brilliant financial modelers who understand it in more depth than I do.)

While some entrepreneurs may somehow possess the bare minimum of skills that are required to create a decent business plan, they most certainly don’t have the time. Starting a business involves numerous steps, and entrepreneurs are often pursuing each of those steps while juggling a full-time career and sometimes a family. It’s a lot.

But a key quality shared by the best leaders is knowing when and what to delegate. If you have a dual major in English and Business, and you’ve done this a few times before, then sure, you could probably write a stellar business plan from scratch.

But if you have virtually any other combination of experience, you could benefit greatly from delegating it to a company like ours that can counsel you every step of the way, scheduling out the project into meetings and discrete tasks so that you can be as involved as you should be in the process while still freeing up your time to handle the many other to-dos on your plate. (This benefit still holds true for the dual major, as well!)

Remember, the most important thing is that the business plan actually gets done so that you can use it to start your business, but like any long writing project, it can fall to the wayside when life’s pressures get in the way. Working with a deadline-driven consultancy like ours can help you reach the finish line.

Now that you have a basic introduction to the traditional business plan document, you probably have plenty of questions that go deeper. We’ve done our best to address those with our frequently asked questions about writing business plans .

How to Write a Management Summary for Your Business Plan

Entrepreneurs are often celebrated for their uncanny ability to understand others – their customers, the market, and the ever-evolving global...

Understanding Venture Debt vs Venture Capital

Despite growth in sectors like artificial intelligence, venture capital funding has seen better days. After peaking at $347.5 billion in 2021, there...

Going Beyond Writing: The Multifaceted Role of Business Plan Consultants

Most people think of a professional business plan company primarily as a "business plan writer." However, here at Masterplans, we choose to approach...

- SUGGESTED TOPICS

- The Magazine

- Newsletters

- Managing Yourself

- Managing Teams

- Work-life Balance

- The Big Idea

- Data & Visuals

- Reading Lists

- Case Selections

- HBR Learning

- Topic Feeds

- Account Settings

- Email Preferences

When Should Entrepreneurs Write Their Business Plans?

- Francis J. Greene

- Christian Hopp

Don’t write a plan before you understand your customer.

It pays to plan. Entrepreneurs who write business plans are more likely to succeed, according to research. But while this might tempt some entrepreneurs to make writing a plan their very first task, a subsequent study shows that writing a plan first is a really bad idea. It is much better to wait, not to devote too much time to writing the plan, and, crucially, to synchronize the plan with other key startup activities.

It pays to plan. Entrepreneurs who write business plans are more likely to succeed, according to our research, described in an earlier piece for Harvard Business Review . But while this might tempt some entrepreneurs to make writing a plan their very first task, our subsequent study shows that writing a plan first is a really bad idea. It is much better to wait, not to devote too much time to writing the plan, and, crucially, to synchronize the plan with other key startup activities.

- FG Francis J. Greene is Chair in Entrepreneurship in the University of Edinburgh Business School.

- CH Christian Hopp is Chair in Technology Entrepreneurship in the TIME Research Area, the Faculty of Business and Economics, RWTH Aachen University.

Partner Center

Want to create or adapt books like this? Learn more about how Pressbooks supports open publishing practices.

2 Developing a Business Plan

Learning Objectives

After completing this chapter, you will be able to

- Describe the purposes for business planning

- Describe common business planning principles

- Explain common business plan development guidelines and tools

- List and explain the elements of the business plan development process

- Explain the purposes of each element of the business plan development process

- Explain how applying the business plan development process can aid in developing a business plan that will meet entrepreneurs’ goals

This chapter describes the purposes, principles, and the general concepts and tools for business planning, and the process for developing a business plan.

Purposes for Developing Business Plans

Business plans are developed for both internal and external purposes. Internally, entrepreneurs develop business plans to help put the pieces of their business together. Externally, the most common purpose is to raise capital.

Internal Purposes

As the road map for a business’s development, the business plan

- Defines the vision for the company

- Establishes the company’s strategy